DeFiTuna: The Journey from Fee Accrual to Revenue Distribution

DefiTuna was the first protocol I started tracking. My dashboards have been live for a while, but I never wrote the companion article explaining how the fee pipeline actually works. After publishing the Flash.Trade fee flow deep dive, it was time to give DefiTuna the same treatment. The fee journey turned out to be surprisingly different: fees arrive in dozens of different tokens from pools across the two supported AMMs, all of which need to be converted to SOL before stakers see a single lamport.

First a note:

- Everything in this article comes from observing on-chain state and transaction data. I have no access to DefiTuna's source code, so the behavioral explanations below are inferences from those traces.

- The mechanics described below are based on on-chain activity observed through March 15, 2026.

Where Does Your SOL Come From?

So, you stake $TUNA. Periodically, SOL appears on your Stake $TUNA page, ready to claim or compound. But where does it actually come from? And how does a fee paid in FARTCOIN for LPing in an Orca whirlpool end up as SOL on your staking page?

I wanted to verify that fees are properly transformed into staker revenue, with nothing materially lost along the way. Without surprise, the pipeline is perfectly accurate. This article walks through how it works.

The Fee-to-Revenue Journey

The diagram on the right shows the high-level path. The first thing to notice: unlike Flash.Trade, which accumulates fees in internal on-chain accounting fields and periodically sweeps them through multiple stages, DefiTuna routes every fee directly to the treasury PDA within the same transaction that generates it. No staging areas, no hourly consolidation. But the fee arrives in whatever tokens the pool trades in, which creates a conversion challenge.

Let's trace a single fee with round numbers. A user deposits 10 SOL as collateral and borrows 20 SOL to open a 3x leveraged LP position on the SOL-USDC Orca whirlpool. DefiTuna's docs describe the protocol fee as a percentage of the borrowed funds amount. That could be a fee of 0.02 SOL of value. Because this is a two-token pool, the fee reaches the treasury split across both tokens: roughly 0.01 SOL and another 0.01 SOL-equivalent in USDC.

The 0.01 SOL is ready for distribution to stakers immediately; it is already in the right denomination. (Technically, the treasury holds it as WSOL, SOL wrapped as an SPL token so it can be handled by the token program like any other token. This article uses "SOL" when talking about value and "WSOL" in technical contexts where the wrapped form matters.) The USDC sits in the treasury's USDC token account, accumulating alongside USDC from dozens of other transactions, until a swap_reward instruction converts the batch to SOL. Then, a deposit_reward instruction deposits all accumulated SOL into the staking contract, where it becomes claimable by TUNA stakers proportional to their stake.

That is the simple case. Now imagine the same fee from a SOL-FARTCOIN pool: half arrives as FARTCOIN. Or from a USDC-WhiteWhale pool: it arrives as USDC and WhiteWhale tokens. Across more than 50 pools and more than 30 different tokens, the treasury is constantly collecting, converting, and depositing.

All treasury revenue is distributed through the staking contract. There is no on-chain split like Flash.Trade's 50/50 split between stakers and a separate protocol-treasury leg; wallets controlled by the team earn through the same staking mechanism as other TUNA holders.

The following sections zoom into each stage of this journey: how fees are charged, how non-SOL tokens are converted, and how SOL reaches stakers.

The Fee Model

DefiTuna is a leveraged liquidity provision protocol. Users deposit collateral, borrow additional capital from DefiTuna's lending pools, and deploy the combined amount as concentrated liquidity on Orca Whirlpools or Fusion AMM pools (for LP positions), or as directional bets (for leveraged spot positions).

An important detail: Fusion AMM is not a third-party AMM. It is built by the DefiTuna team, a hybrid CLMM + on-chain orderbook. Fusion AMM is the underlying trading venue, while DefiTuna is the lending and leverage layer on top. Revenue from both shows up in the same treasury-to-staking pipeline traced here.

DefiTuna charges a protocol fee on position management (opening, compounding, trigger order execution) and a liquidation fee (the docs describe it as 10%) on liquidated positions. The docs illustrate the protocol fee as 0.05% of borrowed funds, but from analyzing 240,000+ scanned treasury transactions I found the most common observed tier is 10 bps (0.10%), with other pools at 5 or 3 bps.

Lenders who supply capital to the lending pools earn borrowing interest. As of this writing, no lending protocol fee appears to flow to the treasury: in the on-chain data I have observed, all borrower interest goes to lenders (as confirmed by the docs).

The swap_reward Conversion Pipeline

Non-SOL tokens accumulate in the treasury's associated token accounts (ATAs) until a swap_reward instruction converts them to WSOL. DefiTuna uses several variants depending on the token and the routing path:

| Instruction | Route |

|---|---|

swap_reward_orca | Single-hop swap via Orca Whirlpool |

swap_reward_fusion | Single-hop swap via Fusion AMM |

swap_reward_two_hop_orca | Two-hop swap via Orca (e.g. FARTCOIN -> USDC -> SOL) |

swap_reward_two_hop_fusion | Two-hop swap via Fusion |

The conversions are part of the same keeper bot cycle as deposit_reward. Every ~3 hours, the bot converts whatever non-SOL tokens have accumulated, down to dust amounts, then decides whether to deposit based on the total WSOL balance (see below). USDC appears in about 99% of conversion cycles because it accumulates fast enough to have a balance every 3 hours. "Niche" tokens like cbBTC (present in about 6% of cycles) may go days between conversions, not because the bot waits for a minimum balance, but because it takes that long for any fees in that token to appear.

The Attribution Puzzle

swap_reward transactions create an accounting challenge. When a conversion turns 100 USDC into 0.7 SOL, that 0.7 SOL is not new revenue. It is the SOL-equivalent of USDC fees that were already earned by earlier transactions. If you count both the original USDC inflow and the swap_reward SOL output, you double-count.

I solve this by tracking a ledger of pending ATA balances per mint and per originating transaction type. When a swap_reward fires, its SOL output is attributed proportionally back to the original transactions that earned the ATA tokens. The conversion itself is never counted as new revenue.

The deposit_reward Cycle

Once fees have been converted to SOL, a deposit_reward instruction deposits the accumulated WSOL into the TUNA staking contract. When deposit_reward fires, it simultaneously updates three fields on the Treasury account: total_reward and total_unclaimed_reward both increase by the exact deposit amount (confirming nothing is skimmed), while acc_reward_per_share increases proportionally. This is the accumulator the contract uses to calculate each staker's claimable share. When stakers call claim_reward, only total_unclaimed_reward decreases. When they compound_reward, it decreases (claimed SOL) and total_staked_shares increases (re-staked).

Every 3 hours, like clockwork

I analyzed all 1,291 deposit_reward events in my dataset to understand the cadence and determine what triggers a cycle.

The base interval is roughly 3 hours. During high-volume periods like October 2025, events fire at near-steady 3-hour intervals. On October 1, the first four events landed at 01:49, 04:50, 07:52, and 10:54 UTC. The gaps are 3h01m, 3h02m, and 3h02m; not exactly 3 hours, but close. The small drift that accumulates over successive cycles suggests a timer-based mechanism rather than a fixed cron schedule.

The trigger threshold is 1.0 SOL. When revenue is low, cycles get skipped. By tracking WSOL inflows to the treasury between consecutive deposits, I found a sharp cutoff: across all 1,291 events, not a single normal deposit fired with less than 1.0 SOL accumulated. The smallest deposits barely cleared the line:

| Event date | Gap | WSOL collected |

|---|---|---|

| 2026-02-10 | 6.1h | 1.003 SOL |

| 2025-11-27 | 3.0h | 1.005 SOL |

| 2026-01-27 | 6.0h | 1.006 SOL |

| 2026-01-04 | 3.0h | 1.007 SOL |

During low-volume periods, skipped cycles become common. In February 2026, only about 37% of inter-deposit gaps were simple ~3-hour intervals. Over the full dataset, the 1,290 gaps between consecutive deposits break down as:

| Gap | Count | Share | Meaning |

|---|---|---|---|

| ~3 hours | 983 | 76.2% | >= 1 SOL available, deposit fires |

| ~6 hours | 227 | 17.6% | One cycle skipped |

| ~9 hours | 53 | 4.1% | Two cycles skipped |

| ~12+ hours | 27 | 2.1% | Three or more cycles skipped |

The behavioral model: every ~3 hours, the keeper checks the treasury's WSOL balance. If >= 1.0 SOL is available, it fires deposit_reward to sweep the full balance into the staking contract. If not, it waits for the next cycle.

What Flows Through the Pipeline

Now that the mechanics are clear, let's look at what actually flowed through this pipeline. Over the 235 days in my dataset (July 24, 2025 to March 15, 2026), the treasury collected 8,381 SOL.

Revenue by Source

| Source | Revenue Type | SOL | Share | What generates it |

|---|---|---|---|---|

| Orca | Leveraged LP | 4,268 | 50.9% | Position opens, closes, liquidations, compounding |

| Orca | Direct transfers | 146 | 1.7% | Revenue collected before the current fee system was in place |

| Fusion | AMM trading fees | 2,544 | 30.4% | collect_protocol_fees sweeps from Fusion pool accounts |

| Fusion | Leveraged LP | 1,339 | 16.0% | Position opens, closes, liquidations, compounding |

| Fusion | Spot positions | 84 | 1.0% | Leveraged spot trading |

| Total | 8,381 | 100% |

The Fusion AMM trading fees deserve a note: collect_protocol_fees is a periodic sweep of accumulated swap fees from Fusion pool accounts. Multiple types of trading activity on Fusion contribute to these fees, but the on-chain instruction aggregates them into a single collection event. Breaking down what trading activity sits behind each sweep would require caching all Fusion pool transactions, not just treasury transactions, which my pipeline currently does not do. There is also a difference in how the two AMMs surface fees: on Orca, fees are collected as part of position management transactions (open, close, compound), while on Fusion, the dedicated collect_protocol_fees sweep is the largest single revenue category.

On both Orca and Fusion, liquidations account for a significant share of LP revenue. This is inherent to leveraged concentrated liquidity: when prices move outside a position's range, the position stops earning fees and becomes increasingly exposed to liquidation risk. With leverage amplifying the losses, positions can hit their liquidation threshold during volatile moves. The liquidation fee (10% per the docs) is substantially larger per event than the protocol fee (typically 10 bps) charged at position opening.

Explore the full breakdown on the revenue by type dashboard.

Revenue by Pool

| Pool | Revenue (SOL) | Share |

|---|---|---|

| Fusion SOL-USDC | 3,053 | 36.4% |

| Orca SOL-USDC | 2,237 | 26.7% |

| Fusion USDC-WhiteWhale | 469 | 5.6% |

| Orca SOL-CBBTC | 344 | 4.1% |

| Orca SOL-FARTCOIN | 303 | 3.6% |

| Other | 1,974 | 23.6% |

SOL-USDC pools on both AMMs account for 63% of revenue, but the remaining 37% comes from a diverse long tail of token pairs. This creates the accounting challenge described in the swap_reward section.

Explore the full breakdown on the revenue by pool dashboard.

The Liquidation Dependency

The data above reveals a structural pattern: DefiTuna's revenue is heavily dependent on liquidations. The protocol fee on position opens is small (typically 10 bps), while the liquidation fee (10% per the docs) generates far more per event.

How much more? Counting all 190,000 revenue events in the dataset (one transaction can contain multiple revenue-generating instructions):

| Category | Events | % of Events | Revenue (SOL) | % of Revenue |

|---|---|---|---|---|

| Liquidations | 8,904 | 4.7% | 4,467 | 53.3% |

| Fusion trading fees | 7,103 | 3.7% | 2,544 | 30.4% |

| LP operations (incl. SL/TP) | 169,735 | 89.5% | 1,140 | 13.6% |

| Spot positions | 3,963 | 2.1% | 84 | 1.0% |

| Other | 3 | 0.0% | 146 | 1.7% |

Nearly 90% of all revenue events are routine LP operations (opens, compounds, fee collections), but they contribute just 14% of revenue. Liquidations are fewer than 5% of events yet account for more than half of all SOL earned. During volatile months like October 2025, liquidation-driven revenue pushed daily totals well above average. During calm stretches like early March 2026, liquidations nearly disappeared and revenue dropped to a fraction.

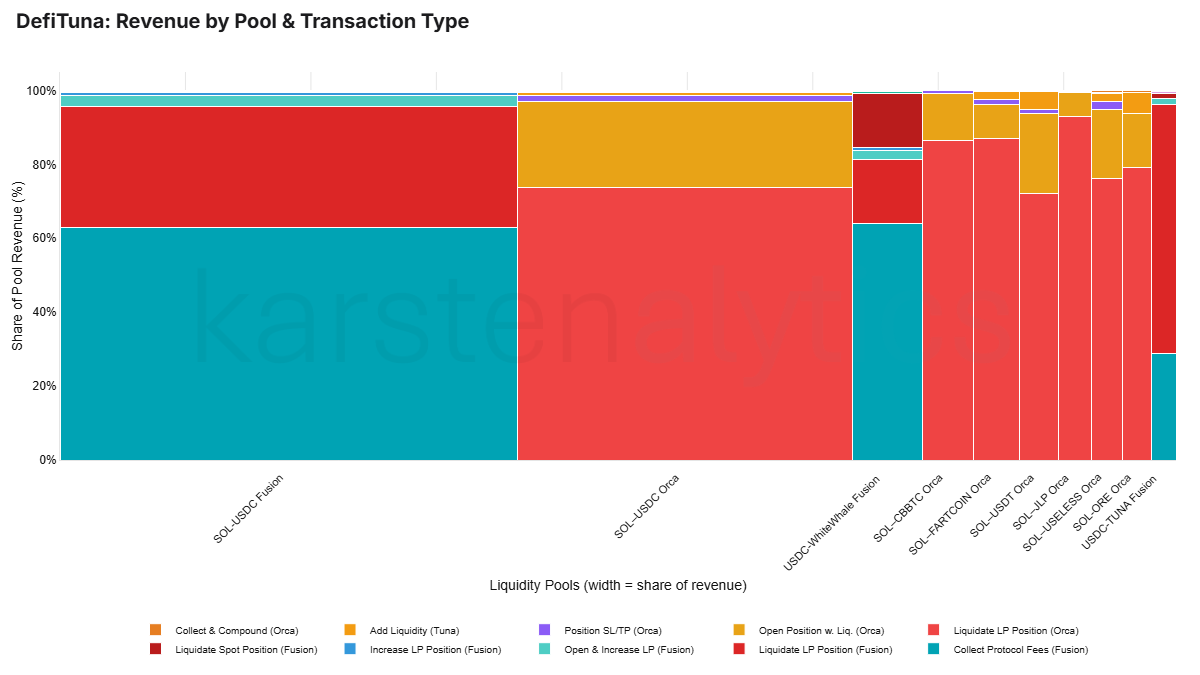

The chart below visualizes this, breaking down the top 10 pools by revenue (covering ~89% of total). Each column is a liquidity pool; column width reflects the pool's share of total revenue. Within each column, colored segments show transaction types, with height indicating their share of that pool's revenue. A large area means a high-revenue combination.

Red segments are liquidation fees. In the Orca SOL-USDC column, red dominates: most of that pool's revenue comes from liquidations. The Fusion SOL-USDC column tells a different story; the largest segment is collect_protocol_fees (teal), the periodic sweep of trading fees from the Fusion AMM. This is the revenue source that does not depend on liquidations. Across the smaller pools on the right, liquidation red is present nearly everywhere.

Interactive version: Revenue by Pool & Transaction Type

A protocol that earns most of its revenue from liquidations needs volatile markets to sustain staker returns.

The DefiTuna team is actively working to change this. They plan to wind down support for Orca pools and consolidate all activity on their own Fusion AMM. That will mean a short-term revenue hit, Orca currently accounts for over 50% of total revenue. But combined with permissionless pool creation on Fusion, which is also in the pipeline, this could fundamentally shift the revenue mix. TUNA staker revenue would become less dependent on liquidations.

But regardless of where the fees come from or how the mix shifts, the pipeline would stay the same: fees arrive in dozens of tokens from LP positions and trading, the keeper bot converts and deposits on roughly three-hour checks, and the revenue ultimately lands in the TUNA staking contract. That is what I set out to verify, and it holds across the full history covered here. The machinery works. What flows through it is the part that will change.

Appendix

Worked Example: February 5, 2026, 04:00-07:00 UTC

An illustrative slice of a 3-hour deposit_reward cycle, focusing on revenue-generating events. This is not a cherry-picked cycle; I simply picked a random date and time window. The transactions shown in Step 1 are a sample of the dozens that occurred during this window, chosen to show the variety of fee sources. Non-revenue treasury operations (staker claims, compounds, lending withdrawals) also occur during the cycle but are omitted here for clarity. All amounts are verifiable on-chain.

The cycle: Between 03:58 and 06:59 UTC, the treasury processed dozens of revenue-generating transactions across multiple pools and token types. At the end of the cycle, a burst of swap_reward conversions and a deposit_reward deposited the accumulated SOL into the staking contract.

Step 1: Fees accumulate from trading activity

Throughout the 3-hour window, fees trickle into the treasury from position management and compounding. A few of the larger events:

| Tx | Time (UTC) | Transaction Type | SOL to treasury | Other tokens to treasury |

|---|---|---|---|---|

| 3ps13...WLifY | 04:11 | Open LP position (Fusion) | 0.009 SOL | -- |

| 4BkQC...HUSc | 05:10 | Open position (Orca) | 0.003 SOL | 0.10 USDC |

| 5LriU...MQtv | 05:53 | Add liquidity (Tuna) | 0.006 SOL | -- |

| 26XVa...S1bB | 06:08 | T/P-triggered close (Orca) | 0.033 SOL | 0.003 JUP |

| 5Ekh8...kWiU | 06:12 | Open position (Orca) | 0.011 SOL | 8.34 JUP |

| 25Aii...4V9 | 06:27 | Open position (Orca) | 0.003 SOL | -- |

The T/P-triggered close at 06:08 is interesting: the canonical instruction is LiquidateTunaLpPositionOrca, but the logs show Executing T/P order, indicating a take-profit trigger rather than a liquidation. The transaction closes the SOL-JUP position, repays the loan, and transfers the protocol fee to the treasury, all in a single transaction.

Step 2: Protocol fees are swept from Fusion pools

At 06:57 UTC, four collect_protocol_fees instructions sweep accumulated fees from Fusion pools in rapid succession:

| Tx | Time | Pool | Token A | Token B |

|---|---|---|---|---|

| 3WMzC...Jre9 | 06:57:53 | SOL-USDC | 0.082 SOL | 7.17 USDC |

| 4mKYK...29Cj | 06:57:56 | USDC-TUNA | 0.73 USDC | 45.79 TUNA |

| 2d9Ni...Y8mU | 06:57:58 | USDC-WhiteWhale | 1.51 USDC | 27.10 WhiteWhale |

| 25vRz...2fhy | 06:58:01 | USDC-PUMP | 0.26 USDC | 187.76 PUMP |

Notice the multi-token nature: these sweeps add USDC, TUNA, WhiteWhale, and PUMP to the treasury's existing token balances, all of which eventually need to be converted to SOL.

Step 3: swap_reward converts token balances to SOL

Immediately after the fee sweeps, five swap_reward transactions fire within 55 seconds, converting the largest accumulated non-SOL balances to WSOL:

| Tx | Time | Instruction | Tokens sold | SOL received |

|---|---|---|---|---|

| 4sN6w...5V7u | 06:58:08 | swap_reward_fusion | 46.95 USDC | 0.521 SOL |

| 3HPwG...9DxS | 06:58:28 | swap_reward_two_hop_orca | 0.0015 cbBTC | 1.186 SOL |

| s5oXN...UeV | 06:58:37 | swap_reward_fusion | 140.72 TUNA | 0.036 SOL |

| 3o4QE...ucB | 06:58:49 | swap_reward_orca | 8.34 JUP | 0.017 SOL |

| 4CFZK...1u1k | 06:59:03 | swap_reward_orca | 0.0039 BTC (Wormhole) | 3.064 SOL |

The amounts sold here reflect balances accumulated over the full cycle, not just the Step 2 sweeps: the 46.95 USDC includes earlier fee inflows, and the cbBTC, JUP, and BTC (Wormhole) come entirely from LP operations earlier in the window. Smaller balances like WhiteWhale and PUMP from Step 2 remain in the treasury for conversion in a later cycle. The cbBTC swap uses a two-hop route (cbBTC -> USDC -> SOL via Orca), while TUNA and USDC are swapped directly on Fusion.

Step 4: deposit_reward credits the staking contract

At 06:59:48 UTC, the deposit_reward instruction (Sk94i...iV8) fires, depositing the accumulated WSOL into the TUNA staking contract. The on-chain log reads:

Program log: total_unclaimed_reward: 1109350827451; acc_reward_per_share: 2625355448996

That is 1,109.35 SOL in total unclaimed rewards across all stakers. The acc_reward_per_share accumulator is what the contract uses to calculate each staker's share; it increases with every deposit and never decreases. Note that total_unclaimed_reward can decrease between deposits when stakers claim or compound, so differencing consecutive values would undercount the actual deposit.

Gross WSOL inflows during this cycle

| Source | SOL |

|---|---|

| Direct WSOL from position mgmt (opens, adds, compounds) | 0.033 |

| Direct WSOL from liquidation | 0.033 |

| Direct WSOL from fee collection | 0.082 |

swap_reward conversions (USDC, TUNA, cbBTC, JUP, BTC (Wormhole)) | 4.823 |

| Total gross inflow | 4.971 |

About 97% of the gross WSOL inflow started as non-SOL tokens and had to be converted first. The actual deposit_reward amount is slightly less: stakers claimed or compounded 0.174 SOL of WSOL from the staking contract during this cycle, reducing the treasury's WSOL balance before the deposit landed.

Revenue data covers July 24, 2025 through March 15, 2026 (235 days). The live version of this data is on the DefiTuna dashboards, updated daily.